Table of Contents

- When Do You Actually Buy Certificates?

- Q: Sales of CBAM certificates haven't started yet. I'm importing CBAM goods in 2026, when do I actually need to buy certificates?

- How Do You Actually Buy Them and Can You Resell Them?

- Log into the CBAM Registry

- Select the number of certificates

- Pay on the Common Central Platform (CCP)

- Q: I bought more certificates than I needed. Can I sell the excess to my sister company who is short?

- What Will Certificates Cost and How Is the Price Set?

- The Certificate Formula: What You Actually Surrender

- The Free Allocation Adjustment : Why Your Obligation Grows Every Year?

- Two tracks: actual vs default

- Carbon Price Already Paid Abroad, Can It Reduce Your Bill?

- Q: My steel supplier is in a country with carbon pricing. They receive some free allowances under that country's ETS. Can I still claim a deduction?

- Q: Is CBAM a new EU tax designed to raise revenue from imports?

- Will CBAM Make Money for the EU And Where Does It Go?

- Summary:

You've heard CBAM is live. But when do you actually buy certificates, what do they cost, how do you surrender them and what happens if the maths goes negative?

Let's be direct: CBAM certificates are money. Each one represents €75–95 (depending on the ETS price) for one tonne of CO₂ embedded in your imports above the EU benchmark. If you import steel, cement, aluminium, fertilisers, or hydrogen into the EU. This blog is where the actual bill gets calculated.

The EU published its official Questions & Answers document (last updated 27 May 2026), and Chapter 3 covers everything about certificates, from when you buy them to what happens if the number turns negative. Let's unpack every question with running case study.

When Do You Actually Buy Certificates?

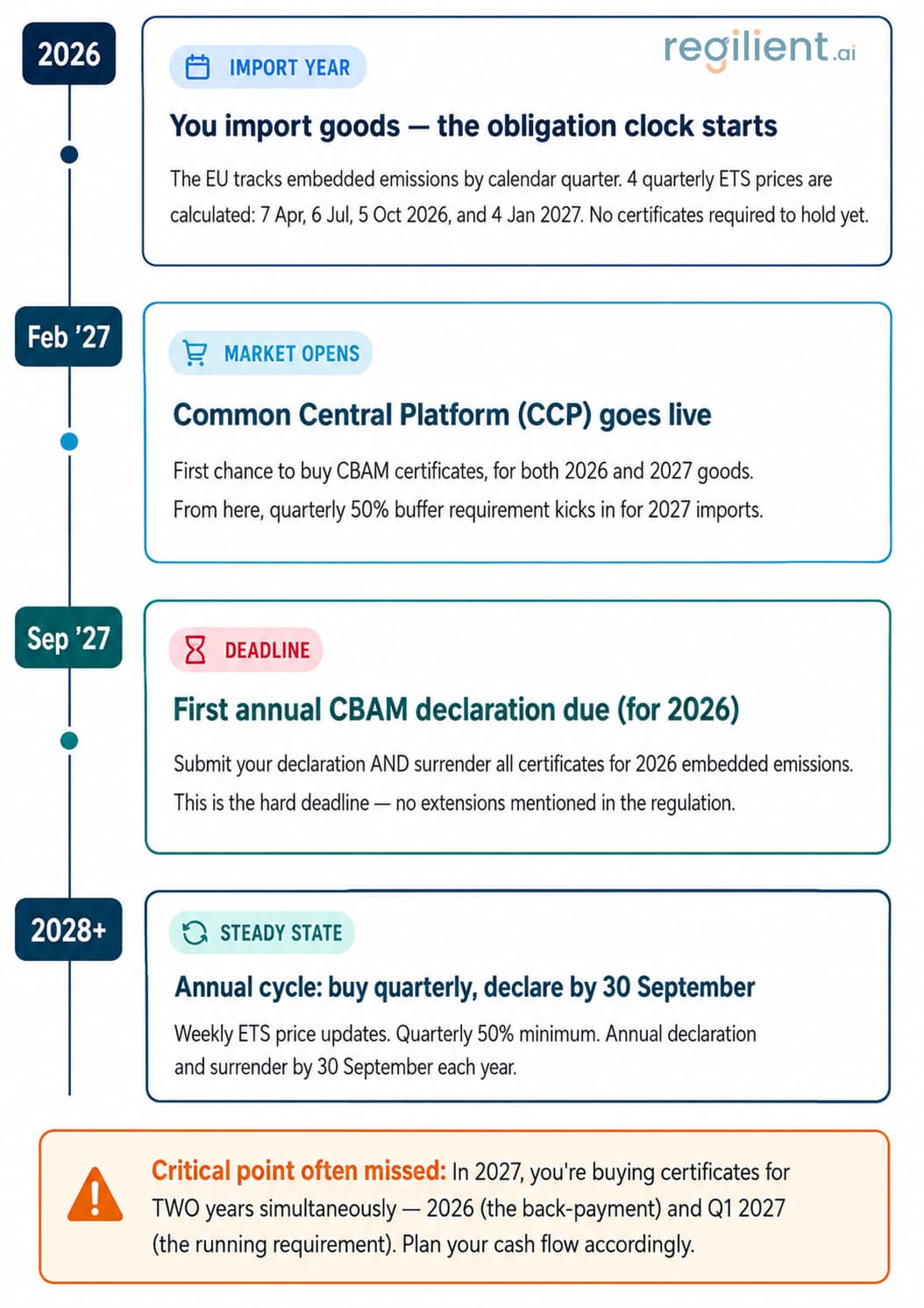

This is the question everyone asks first and the answer has a deliberate quirk: you buy the 2026 certificates in 2027. Here's why, and here's the full timeline.

Q: Sales of CBAM certificates haven't started yet. I'm importing CBAM goods in 2026, when do I actually need to buy certificates?

Certificate sales start on 1 February 2027. For 2026 imports, you'll buy the corresponding certificates on the Common Central Platform (CCP) between February and 30 September 2027. The price you pay will be based on the quarterly average ETS auction price for each quarter of 2026, not a single 2026 price.

From 2027 onwards, you must also maintain a running buffer: every quarter, you must hold certificates covering at least 50% of your year-to-date emissions. Deadlines: 31 March, 30 June, 31 October, 31 December.

How Do You Actually Buy Them and Can You Resell Them?

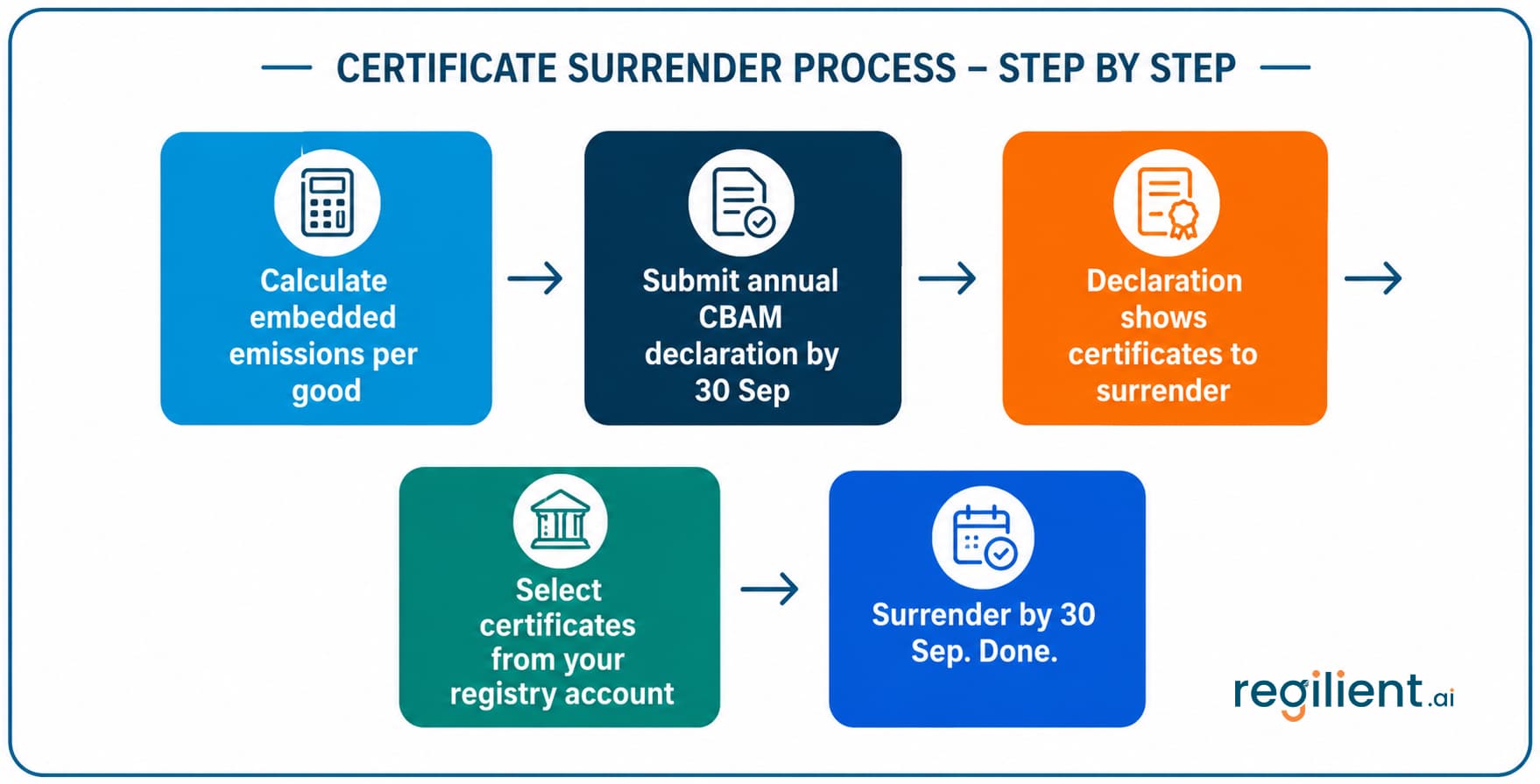

The buying process is deliberately centralised and tied to your identity as an authorised declarant. Think of it less like an exchange and more like a government counter with ID check included.

Log into the CBAM Registry

Only authorised CBAM declarants have access. You'll see your CBAM account number and a certificate purchase screen.

Select the number of certificates

Enter how many you want to buy. Price, currency, and calculations fill in automatically no mental arithmetic required.

Pay on the Common Central Platform (CCP)

The registry redirects you to the CCP for payment. You provide payment details and complete the transaction.

Q: I bought more certificates than I needed. Can I sell the excess to my sister company who is short?

No. CBAM certificates cannot be transferred or sold to another person, not even to an entity in the same corporate group. They are single-use instruments tied to the purchasing declarant.

Excess certificates are only ever: (a) surrendered by you, (b) repurchased by the Member State where you're established, or (c) cancelled by the Commission. There is no secondary market.

Certificates appear in your registry account

Back to the CBAM Registry. Certificates are now on your account and available for surrender.

What Will Certificates Cost and How Is the Price Set?

The short answer is whatever the EU ETS costs that week or quarter. CBAM certificates are priced to exactly mirror the allowances that EU producers buy on the ETS ensuring no competitive advantage from importing.

"The price of CBAM certificates will mirror the ETS allowance price ensuring importers are treated in an even-handed way compared to EU producers."

2026: Quarterly pricing

For 2026, the Commission calculates the certificate price four times, using the average auction clearing price of EU ETS allowances. Dates are fixed in regulation:

2027 onwards: Weekly pricing

From 2027, the Commission publishes a weekly price, the average closing price of ETS allowances (not auction price). Both calculations are volume-weighted to better reflect true market conditions. Published every week, available on the CBAM website.

Note: As of early 2026, EU ETS prices have been trading in the €60–90/tCO₂ range. Regilient's cost calculator uses indicative estimates of €80 (2026), €85-€90 (2027), and €100 (2028+), update these with live prices for accurate forecasting.

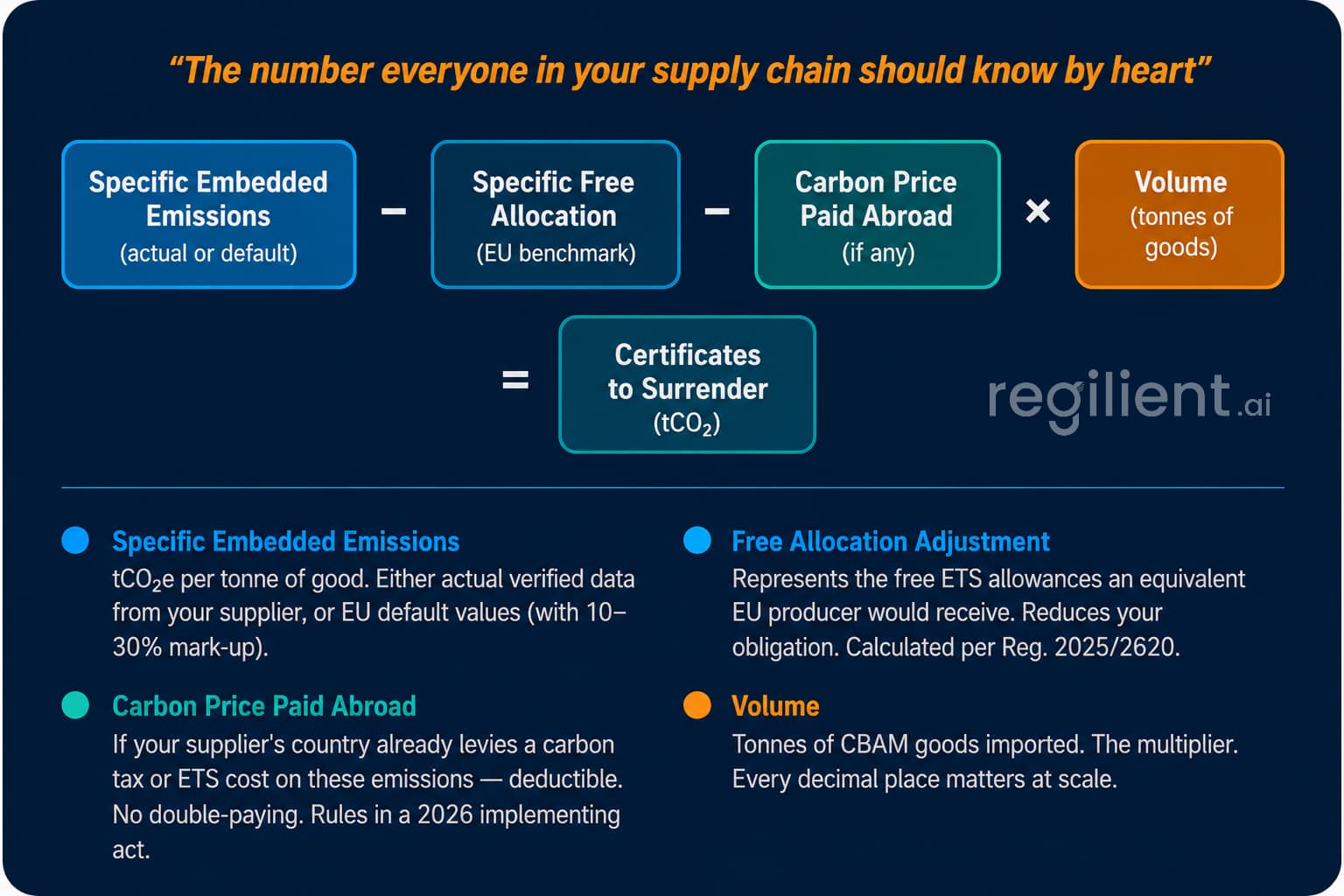

The Certificate Formula: What You Actually Surrender

This is the heart of CBAM. The number of certificates to surrender is not simply "your emissions × ETS price". There are three deductions and getting them right can mean the difference between a seven-figure liability and a much smaller one.

Q: What if the formula gives me a negative number? Do I get a refund?

No refund but also no obligation. If the calculation produces a negative number (e.g., because the carbon price already paid abroad exceeds the EU ETS price, or embedded emissions are below the free allocation), that good's CBAM liability is simply set to zero.

Crucially, that negative value cannot be applied to offset other goods in your declaration. Each CN code is calculated independently.

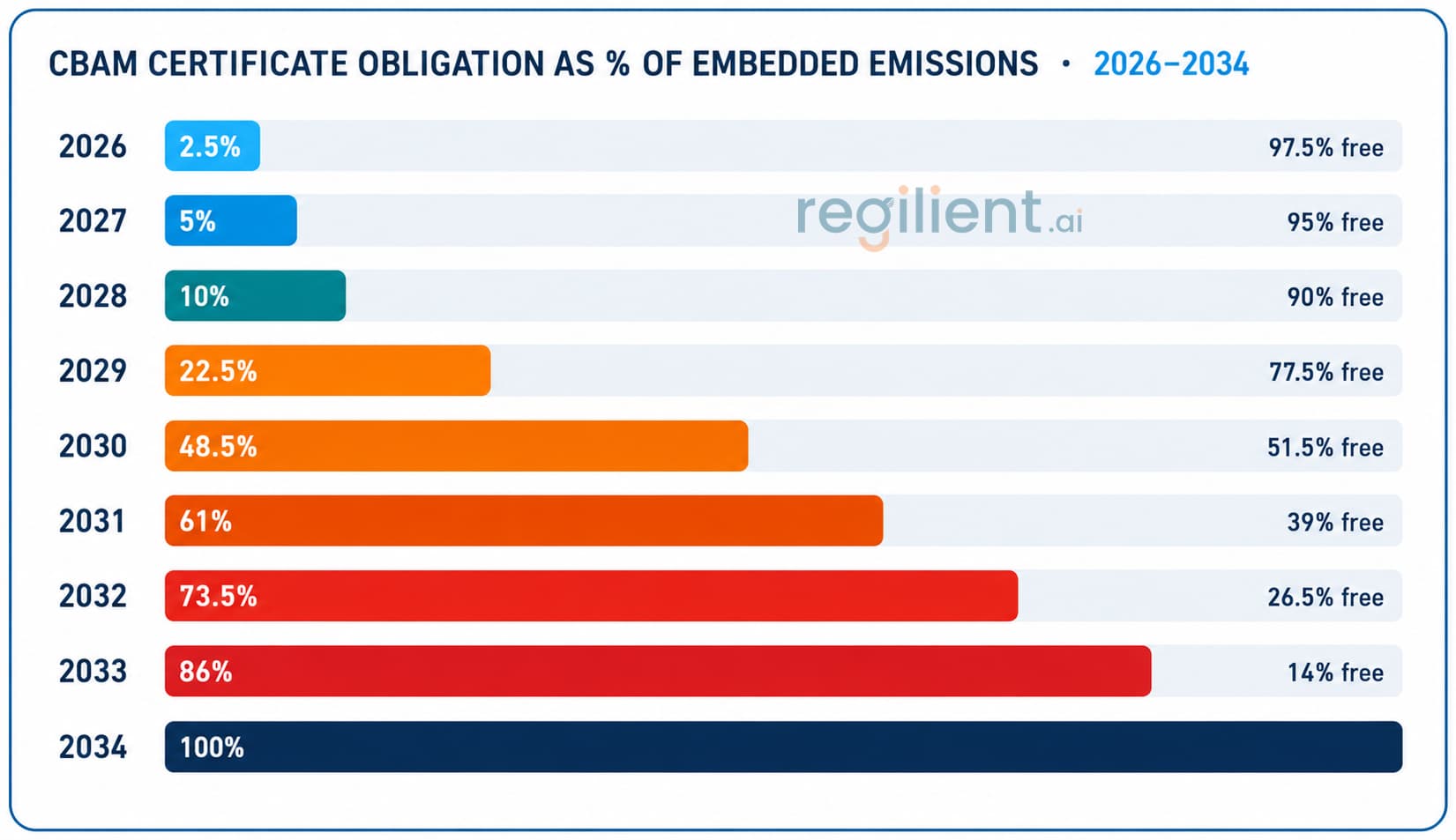

The Free Allocation Adjustment : Why Your Obligation Grows Every Year?

Here's the mechanism that makes CBAM a ticking clock rather than a fixed cost. EU producers currently receive free allowances under the ETS meaning they don't pay for some of their emissions. CBAM mirrors this: your certificate obligation is reduced by the equivalent of those free allowances.

But those free allowances are being phased out. And as they disappear, your CBAM obligation grows proportionally.

Two tracks: actual vs default

The free allocation calculation follows the same track as your emissions reporting:

If you use | Free allocation basis | Which benchmark applies |

Actual verified emissions | Actual free allocation reflects the real production process and composition | Column A benchmarks (Reg. 2025/2620): process-related, without precursors |

Default values | Default free allocation based on standard assumptions | Column B benchmarks (Reg. 2025/2620): includes precursors. Same production route as in Reg. 2025/2621. |

Note: For electricity imports, there is no free allocation in the EU ETS, so there is no free allocation adjustment to CBAM liability for imported electricity either.

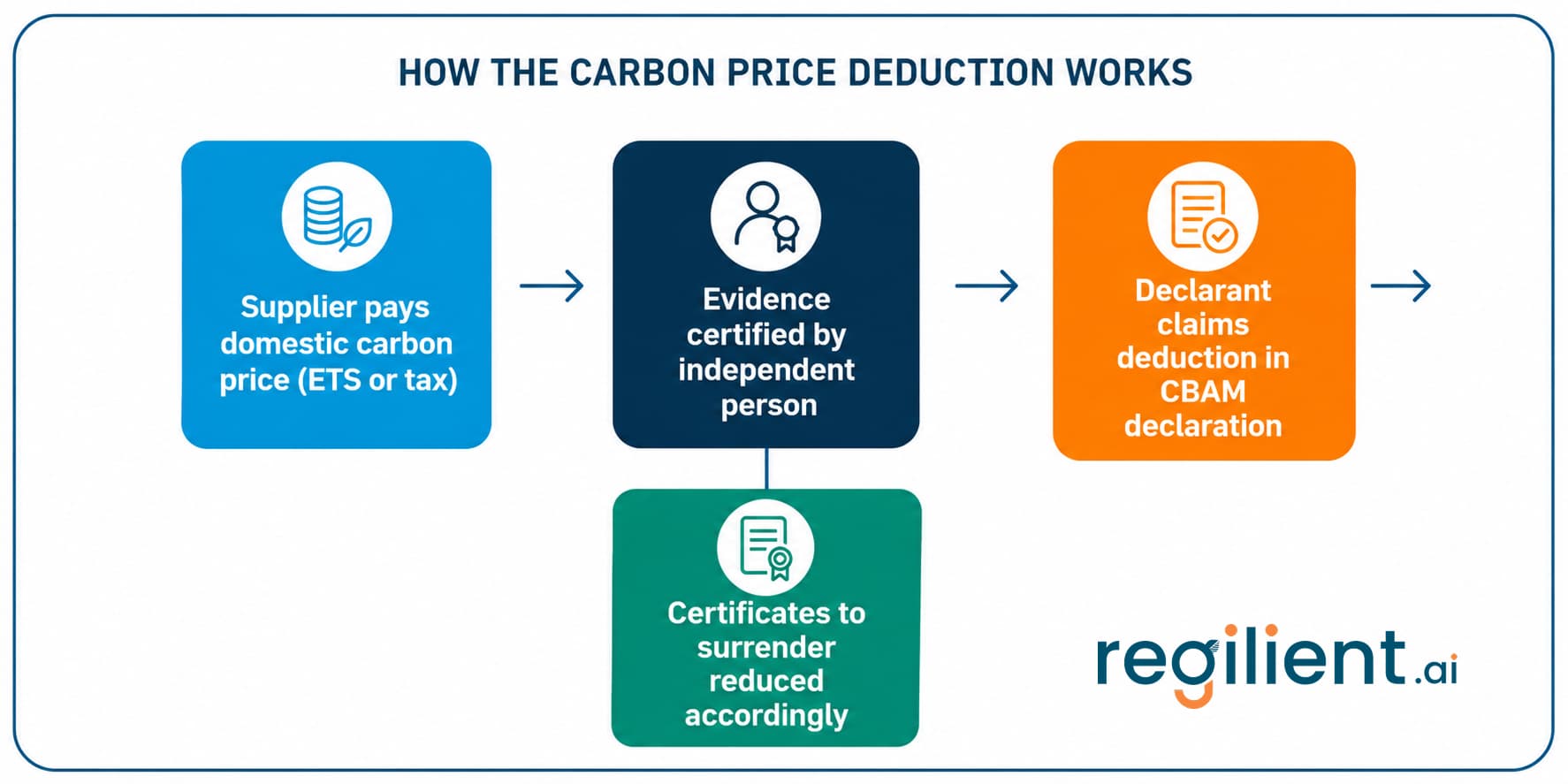

Carbon Price Already Paid Abroad, Can It Reduce Your Bill?

Yes and this is one of the most practically important provisions for importers from countries that already have carbon pricing (think certain Canadian provinces, China's national ETS, South Korea, or UK carbon market). The idea is simple: if your supplier already paid a carbon price, you shouldn't pay again for the same emissions.

Q: My steel supplier is in a country with carbon pricing. They receive some free allowances under that country's ETS. Can I still claim a deduction?

Only on the carbon price that was effectively paid, meaning after free allowances and rebates are netted out. If your supplier received free allowances covering 40% of their emissions, only 60% of the carbon price counts as "effectively paid".

The Commission is adopting a detailed implementing act in 2026 covering: evidence rules, currency conversion (at yearly average exchange rates), what counts as a rebate or compensation, and certification by an independent person.

There will also be default carbon prices per country, a fast track similar to default emission values, allowing declarants to claim a standard deduction without needing certified evidence for every shipment.

Q: Is CBAM a new EU tax designed to raise revenue from imports?

No, and the EU is explicit about this. CBAM is not designed to generate budgetary revenue. Its purpose is to level the carbon playing field between EU and non-EU producers, and to incentivise third countries to introduce their own carbon pricing.

The Commission expects that successful CBAM implementation will actually reduce revenues over time, because it should motivate exporters to decarbonise (thus lowering embedded emissions) and trading partners to price carbon domestically (enabling deductions that reduce CBAM obligations).

That said, if revenues do materialise, especially in early years, they become an own resource for the EU's budget under interinstitutional agreement LI 433/28. But this is treated as an ancillary effect, not the goal.

Will CBAM Make Money for the EU And Where Does It Go?

This question matters for the cynics in the room who wonder if this is a revenue-grab dressed up as climate policy. The honest answer is nuanced.

Note: CBAM creates a strong incentive for trading partners (Turkey, India, China, Brazil) to implement domestic carbon pricing. Once their carbon price equals the EU ETS price, the CBAM deduction eliminates the entire CBAM obligation and their manufacturers keep the revenue domestically rather than paying it to EU.

Summary:

Question | The answer in plain terms |

When do you buy? | CCP opens 1 Feb 2027. Buy 2026 certs by 30 Sep 2027. From 2027, 50% quarterly buffer. |

Where do you buy? | Common Central Platform (CCP), accessible only via the CBAM Registry. Declarants only. |

Can you sell surplus? | No. Certificates are non-transferable. Excess certificates can be repurchased by Member State or cancelled. |

What's the price? | Mirrors EU ETS. Quarterly in 2026 (4 fixed dates). Weekly from 2027. Volume-weighted average. |

How many must you surrender? | (Emissions − Free allocation − Carbon price abroad) × Volume. Never negative — floor is zero. |

What reduces your bill? | 1) Actual verified emissions (vs high defaults). 2) Free allocation mirror. 3) Carbon price deduction. |

Does CBAM raise revenue? | Not by design. Any revenues go to EU own resources. Goal is decarbonisation, not taxation. |

Calculating what you actually owe under CBAM means tracking ETS prices, free allocation phase-outs, and carbon price deductions simultaneously, for every shipment. Book a Regilient demo to see how Regilient automates the full CBAM certificate calculation, from emissions reporting through to surrender.